Investors and policymakers have been obsessed with the risk of deflation for so long that they may be missing the risk of higher inflation. The headline inflation numbers in the U.S. do in fact signal a deflationary impulse. Prices have contracted by 0.20% over the last twelve months, but the headline number is being depressed by lower gas prices and a stronger dollar. Neither factor will persist indefinitely. Services inflation, which is a more stable indicator of inflation, shows that the underlying trend of inflation is up.

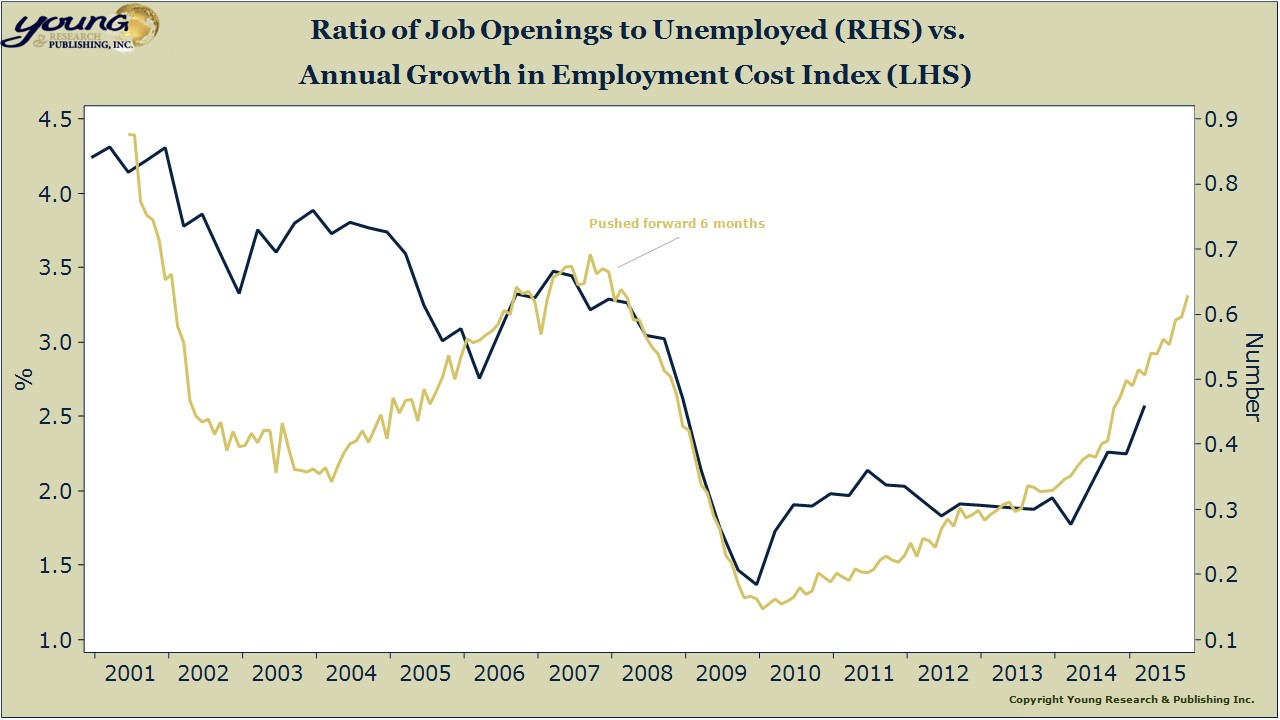

Trends in the labor market are also pointing toward higher prices. The ratio of job openings to the number of unemployed workers is closing in on prior cycle highs. When the ratio of job openings to those seeking a job rises, wage pressure builds which feeds in to inflation.

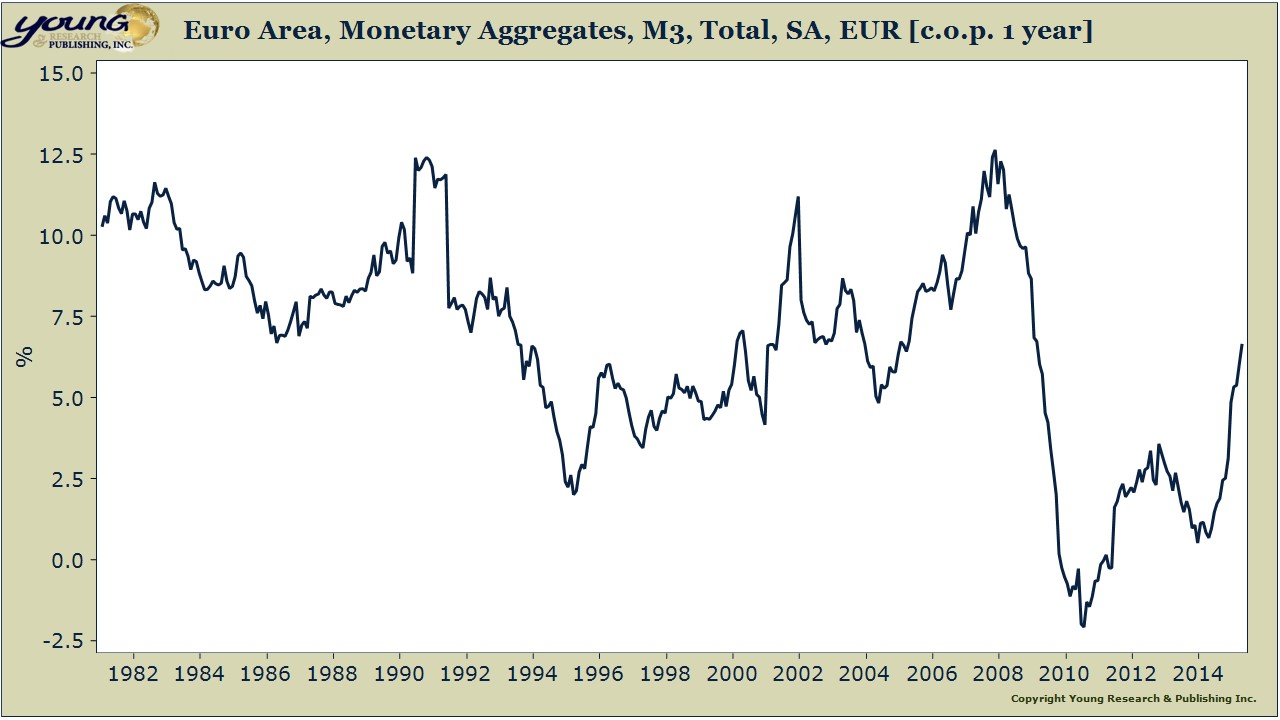

The final indicator that points toward a potential surprise in inflation is money supply growth in the euro-area. Money growth and inflation are tied at the hip. Milton Friedman said inflation is always and everywhere a monetary phenomenon. With money growth soaring in the euro-area, persistent deflation is likely off the table there. Less euro-area deflation likely means faster inflation in the U.S.