Originally posted May 22, 2015.

(See Part II by clicking here).

With long-term interest rates rising sharply in recent weeks, many investors are wondering what they should be doing with their bond holdings.

How do bonds perform in a rising interest rate environment?

That answer of course depends on the type of bonds you own. Are they short-maturity bonds or long-maturity bonds. Are they corporate bonds, Treasury bonds, or mortgage backed securities? What are the ratings of the bonds? Are they dollar denominated bonds or foreign currency denominated bonds?

Lots of variables to think about and too many to cover in this post. So I’ll instead focus on one class of bonds that many investors own and are not fully understood. That class of bonds I am talking about is mortgage backed securities (MBS).

What is the outlook for mortgage backed securities and in particular GNMA Mortgage Backed Securities?

To formulate an outlook for GNMA securities it is necessary to first understand them. GNMA securities are mortgage-backed securities. Mortgage-backed securities are bonds backed by payments on mortgage loans. The loans are pooled and then out of those pools securities are issued that entitle holders to a share of interest and principal. GNMA’s are the only mortgage-backed securities that are explicitly backed by the full-faith and credit pledge of the United States government.

GNMA Securities vs. Conventional Bonds

Mortgage-backed securities are not like conventional bonds. Conventional bonds pay interest during the life of the bond and all principal at maturity. Mortgages pay principal and interest every month in varying amounts. Most investors intuitively understand this. When you take out a mortgage, you make a payment each month that includes interest and principal. When you refinance your mortgage, you are making what is called a pre-payment.

Pre-Payment Risk

Because GNMA securities are backed by the U.S. government, they are free of credit risk, but they do carry pre-payment risk and extension risk. Pre-payment risk is the risk that your principal will be repaid before maturity. Why is getting paid early a risk?

Let’s say you invest in a GNMA security and every mortgage backing that security has a 6% rate. Fast-forward one year and assume that mortgage rates have fallen to 4%. Further assume that every mortgage backing the GNMA security is refinanced to lock in that lower 4% rate. As the investor in this GNMA security, the entire balance of your principal is returned to you. You can reinvest in another GNMA security, but the prevailing rate on GNMA securities is now only 4%. Instead of earning 6% on your money, you now earn 4%.

Extension Risk

Extension risk is the opposite of pre-payment risk. When interest rates rise, the rate of pre-payments on GNMA securities slows, which effectively extends the maturity of a GNMA security. You now have a longer maturity bond than you originally invested in just as interest rates are rising. The combination of higher rates and a longer maturity results in a lower price.

While interest rates are the big factor that determines the percentage of a pool of mortgage backed securities that is paid back ahead of maturity, it is not the only factor. The rate of pre-payments on a pool of mortgages also depends on the historical path of interest rates, housing turnover, the aging of loans, seasonality, and credit conditions among other factors.

In return for taking on pre-payment risk and extension risk, investors in GNMA securities are compensated with yields that are greater than the yields on Treasury securities. How much greater varies over time and by measurement.

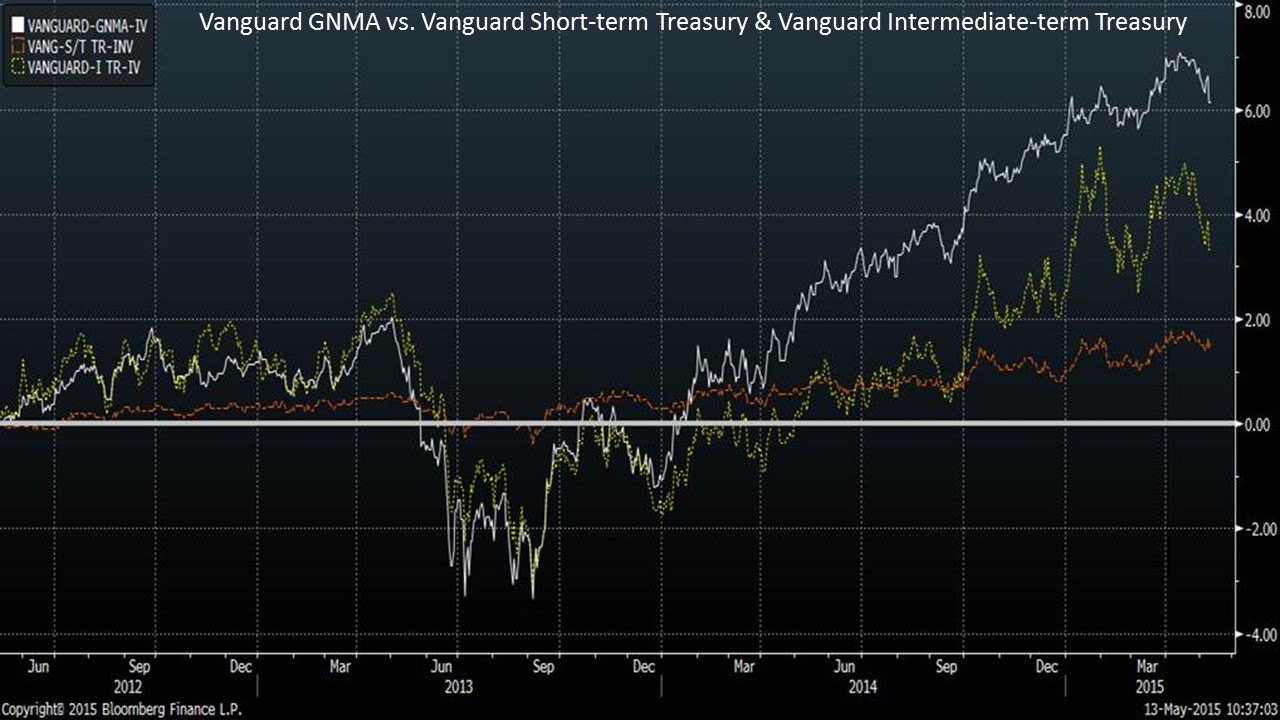

Over the last three years, taking pre-payment and extension risk has been a winning strategy. The Vanguard GNMA fund earned about 0.90% more per year than the Vanguard Intermediate-term Treasury Fund and 1.60% more per year than the Vanguard Short-term Treasury fund.

Now that you have a better understanding of GNMA securities, you are better positioned to understand the outlook for Vanguard GNMA which we will cover next week.