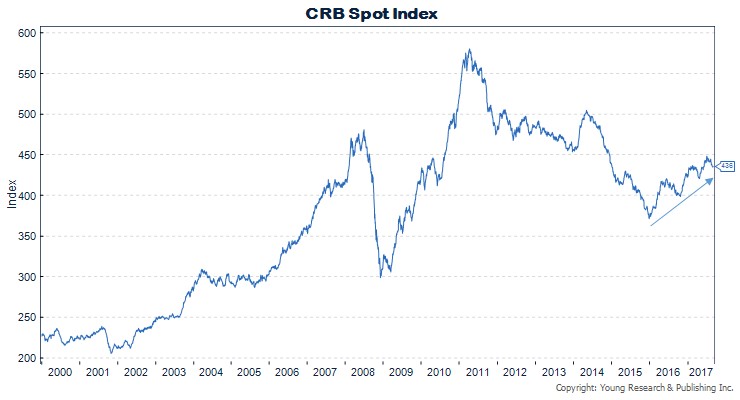

Since early 2016, commodities prices have been making up some of their massive post-2011 losses (see chart below). Some of the increase in commodity prices is thanks to strong demand. More of the increase relies on dollar weakness and Chinese stimulus plans. At the FT, John Authers explains the current bullishness in commodities.

The US stock market has outstripped the rest of the planet ever since the financial crisis. But rising raw materials prices historically help the rest of the world outperform the US.

That did not happen when metals prices rallied in the wake of the crisis — but that could easily be explained by the sovereign debt crisis that gripped the eurozone. From 2012, a bear market for raw materials ensured that the rest would lag behind the US once more. But the current recovery in materials prices has not, as yet, been matched by a major reverse for the trade in which US stocks beat the rest of the world.

It has, however, seen a significant weakening of the US dollar. If we believe the markets, growth is being driven by China, not the US. What happens next relies mainly on the actions of politicians in the US and China.

If the US can agree on a big fiscal stimulus, and return to the protectionist agenda on which President Donald Trump was elected, then a recovery for the dollar is likely. If the US does not manage to opt for economic nationalism as once expected, and if the Chinese leadership does not opt to slow down later this year once it has passed its own political road bump, then we should expect non-US assets to outperform significantly.

Read more here.