Economists Amar Bhidé and Edmund Phelps excoriate the Fed for its handling of the recovery in a recent Wall Street Journal editorial. Bhidé and Phelps say that neither of the Fed’s intended goals of boosting wealth or confidence have likely been achieved.

[I]n late 2008 the Fed began its policy of “quantitative easing”—repeated purchases of billions in Treasury debt—aimed at speeding recovery. “QE2” followed in late 2010 and “QE3” in autumn 2012. Fed Chairman Ben Bernanke said in November 2010 that this unprecedented program of sustained monetary easing would lead to “higher stock prices” that “will boost consumer wealth and help increase confidence, which can also spur spending.”

It is doubtful, though, that quantitative easing boosted either wealth or confidence. The late University of Chicago economist Lloyd Metzler argued persuasively years ago that a central-bank purchase, in putting the price level onto a higher path, soon lowers the real value of household wealth—by roughly the amount of the purchase, in his analysis. (People swap bonds for money, then inflation occurs, until the real value of money holdings is back to where it was.)

Bhidé and Phelps go on to point out that not only has the Fed failed to achieve its goals, but it may have made the situation even worse.

Moreover, the Fed’s quantitative easing appears not to have increased confidence and may have reduced it. No one—the Fed included—knows how much more it will buy or how much of its mountain of Treasurys will be sold back to the market. The Fed said it would end easing at serious signs of faster inflation. But as the housing bubble that preceded the financial crisis showed, imprudent speculation can be destructive without high inflation. Today we have banks, insurance companies and pension funds leveraging their assets and loading up on credit risks because prudence cannot provide acceptable returns.

The cost of this uncertainty can be considerable. An attendant foreboding may lie behind some of the depression in business investment—even if myopic traders in bonds and currencies are impervious to it and too-big-to-fail banks go on making one-way bets. Also, the time and money that businesses give to innovation and efficiency gains are squeezed if the businesses are distracted by the uncertainties surrounding monetary policy.

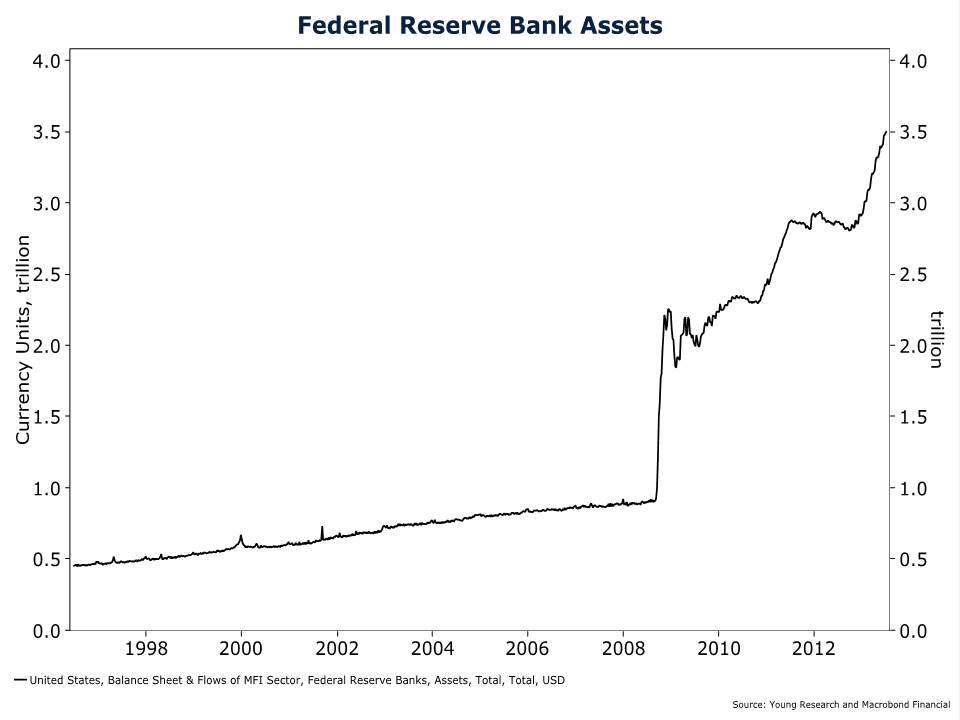

If you take a look at the chart below of Federal Reserve Bank Assets, you’ll begin to understand that any attempt to reverse course could make the situation even worse. Trying to unwind the massive balance sheet that has been accumulated after all these failed attempts at quantitative easing will be extremely difficult.

Bhidé and Phelps conclude with a call for the Federal Reserve to return to its original mission, which they call its “foundational aims.” We agree wholeheartedly that this would be an improvement upon the current system.

Congress passed the Federal Reserve Act in 1913 mainly to forestall and contain panics, discourage speculation and improve the supervision of banks, not to steer the economy. Indeed, the Federal Reserve System was set up as 12 more-or-less independent reserve banks to assuage concerns about centralized control and capture by financial interests.

Restoring the modest foundational aims and diffused governance of the Fed would be good for our economy and good for our democracy.