When asked about the effectiveness of quantitative easing at a University of Michigan forum recently, Federal Reserve Chairman Ben Bernanke gave a curious and terrifying answer. It was curious for how forthright it was. It was terrifying because if the Fed already knows the answer, then their actions seem all the more unjustified.

When asked about the program’s effectiveness Bernanke said “So far, we think we are getting some effect, it is kind of early. We are going to continue to assess how effective [the program is] because it is possible that as you move through time and the situation changes that the impact of these tools could vary.”

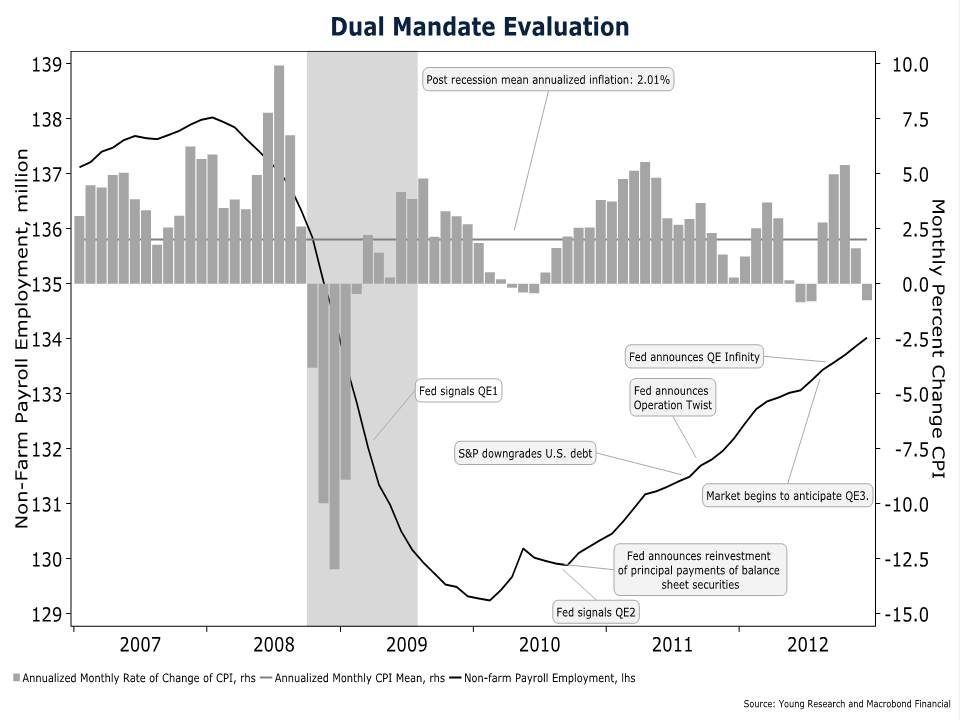

Kind of early? As you can see on the chart nearby QE1 began in 2009 and QE2 in 2010. Three and four years later Bernanke still thinks it’s too early to assess effectiveness? Perhaps after he leaves the Fed and returns to the protected citadel of academia it will be time to assess his tenure as Fed Chairman. Until then, Bernanke prefers we not judge his schemes.

Let’s look at the effectiveness. The Fed has a dual mandate to foster employment and to keep inflation low, Bernanke has made that quite clear. Since QE began, average annualized inflation has been 2.01%, right on the Fed’s target. But five years after employment began to collapse at the beginning of 2008, and four years after the beginning of QE1, employment is still 4 million jobs below its prerecession high. And every year more students have graduated looking for work, and more baby boomers have decided not to retire because they can’t afford to. If, after four years, QE hasn’t created jobs, why would it be effective today?

But rather than admit defeat, the Fed is prepared to push on with QE until it appears to work. We say “appears” because eventually the economy will mend itself. That’s what markets do. At that point, more than four years too late, the Fed is sure to take credit for the smashing recovery it has engineered. Chicago Fed President Charles Evans laid out just this scenario for anyone who was listening on Sunday. He said only “substantial improvement” in labor markets would be enough for the Fed to consider ending QE. The necessary conditions would be “on the order of 1 million to 1.5 million jobs over the next six months to a year. That would be indicative that we could stop.” So once the economy shows improvement, the Fed will declare victory without acknowledging its multi-year failure to encourage growth by money printing.

In the last four and half years the Federal Reserve has unleashed the most aggressive monetary policy in the country’s history without a clue as to what to expect. The strategy for the Fed was, “Ready, fire, aim!” Without a shred of evidence that QE has helped to put people back to work in four years, the Fed presses onward with the same policy. More of the same will surely work this time, right?