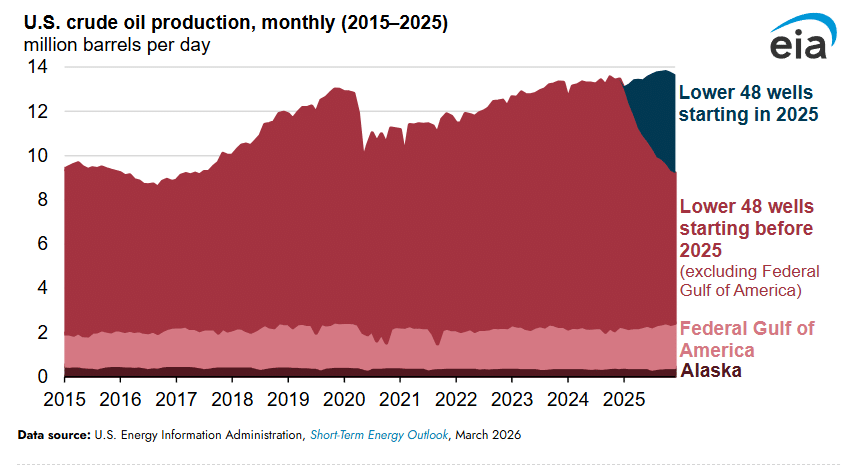

US crude oil production reached a record 13.6 million barrels per day (b/d) in 2025, up 3% from 2024, according to the US Energy Information Administration’s March 2026 Short-Term Energy Outlook.

Most production came from the Lower 48 states (11.3 million b/d), with the Permian Basin driving growth (+280,000 b/d). Despite fewer rigs and wells, efficiency gains supported higher output.

Production in the Eagle Ford and Bakken remained largely flat, while Gulf of America output rose to 1.9 million b/d thanks to five new projects coming online. Lower breakeven prices in key basins supported continued investment and production. The EIA writes:

U.S. crude oil production grew by 3%, or 350,000 barrels per day (b/d), in 2025, setting a new annual production record of 13.6 million b/d, according to our latest Short-Term Energy Outlook (STEO). Production from the Lower 48 states excluding the Gulf of America (L48) accounted for 11.3 million b/d, or 83% of the total U.S. crude oil production in 2025. The rest of the production came from Federal Gulf of America (GOA) and Alaska.

In 2025, the number of active rigs per month in L48 was 5% less than in 2024 and 1% fewer wells were drilled. Despite less rig activity and fewer wells, efficiency improvements that we saw in 2024 continued through 2025 and resulted in a slight increase in crude oil production, with new wells producing 2.9 million b/d of crude oil and wells drilled prior to 2025 producing 8.3 million b/d. Rig and well activity fell in 2025 compared with 2024 because West Texas Intermediate (WTI) crude oil prices fell from $77/barrel (b) in 2024 to $65/b in 2025.

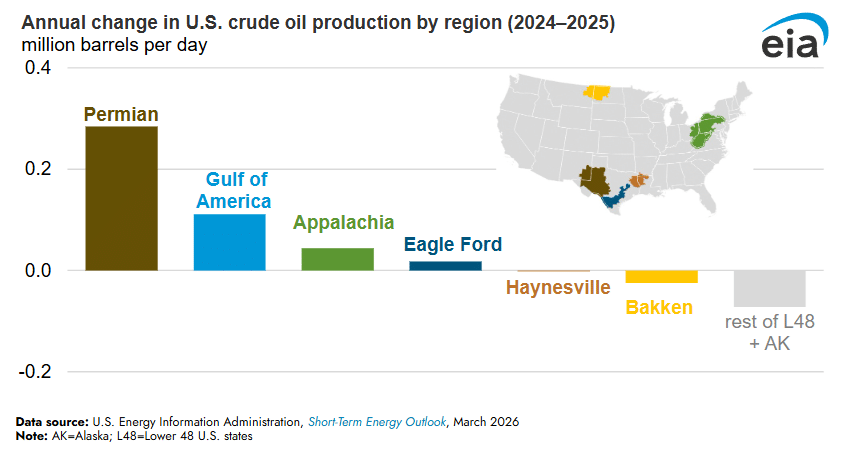

We break out L48 crude oil production for the Appalachia, Bakken, Eagle Ford, Haynesville, and Permian regions in the STEO. The Permian, Eagle Ford, and Bakken are the most prolific crude oil production regions, accounting for almost two-thirds of total U.S. production.

In 2025, the Permian region in western Texas and southeastern New Mexico produced more crude oil than any other region, accounting for 48% of total U.S. crude oil production. Most of the annual U.S. crude oil production growth in 2025 also came from the Permian, where production grew by 280,000 b/d to 6.6 million b/d.

Oil industry executives responding to the Dallas Fed Energy survey reported the two largest basins in the Permian had breakeven prices of $61/b (Midland Basin) and $62/b (Delaware Basin) in 2025. These prices were lower than the annual average of $77/b, encouraging crude oil production. Executives more recently reported slightly higher breakeven prices.

The Eagle Ford (south Texas) and Bakken (North Dakota and Montana) regions each contributed 9% of the total U.S. crude oil production in 2025, similar shares compared with 2024 production. Overall production in these regions remained mostly flat. Eagle Ford production rose 1.6% (18,000 b/d) to 1.2 million b/d in 2025. Bakken production fell by 30,000 b/d to 1.2 million b/d.

Crude oil production in GOA increased by 111,000 b/d in 2025, averaging 1.9 million b/d for the year. Five new GOA projects—Whale, Ballymore, Dover, Shenandoah, and Leon-Castile—came online in 2025. Production in GOA is driven by many factors, such as water depths, resource sizes, and development costs. Because of the long lead times from development to completion, crude oil prices have little impact on production in the short term.