The next time you see an advertisement for an absolute return fund, make sure you do your homework and understand exactly what you’re getting yourself into. I’ve been digging through the 100-plus prospectus pages of the Putnam Investments Absolute Return suite of funds and can tell you the reading isn’t as straightforward as I’d like it to be. Even in the reduced format of the Putnam Absolute Return 100 Fund’s summary prospectus 2/28/11 (only seven pages), there’s some mind-numbing small print.

The next time you see an advertisement for an absolute return fund, make sure you do your homework and understand exactly what you’re getting yourself into. I’ve been digging through the 100-plus prospectus pages of the Putnam Investments Absolute Return suite of funds and can tell you the reading isn’t as straightforward as I’d like it to be. Even in the reduced format of the Putnam Absolute Return 100 Fund’s summary prospectus 2/28/11 (only seven pages), there’s some mind-numbing small print.

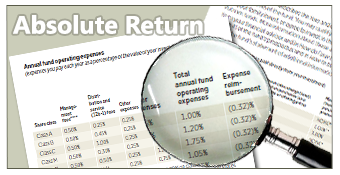

Here’s what I gather you’re up against for the Class A shares: a 1% sales load (charged at the time of purchase), a yearly management fee of 0.50%, a distribution and service (12b-1) fee of 0.25%, and other expenses of 0.25%, for a total operating expense of 1%. So for year one, the total fee is 2% of your assets. But management has decided to offer a reimbursement, so there’s a 0.32% break, bringing it down to 1.68% in year one.

The goal of the Putnam Absolute Return funds is to pursue a rate of return that exceeds inflation, as reflected by Treasury bills, by 100, 300, 500, or 700 basis points—hence the names Absolute Return 100, 300, 500, and 700. With Treasury bills yielding 0.05%, that’s not much of a hurdle, wouldn’t you agree? And so what if the fund hopes to return a certain number of points above Treasury bills? That doesn’t mean it will.

Absolute funds can’t promise anything more than any other fund. They just use a different marketing technique. It’s amazing to me how much of a marketing machine the mutual fund industry continues to be. It not only comes out with new products that fit the mood of the market, but is also able to distribute products to the individual investor through massive captive channels like 401(k)s. The selection of mutual funds offered by most 401(k)s is a lot like cable television. You get hundreds of stations to choose from, and still have nothing good to watch.

{kind=link}