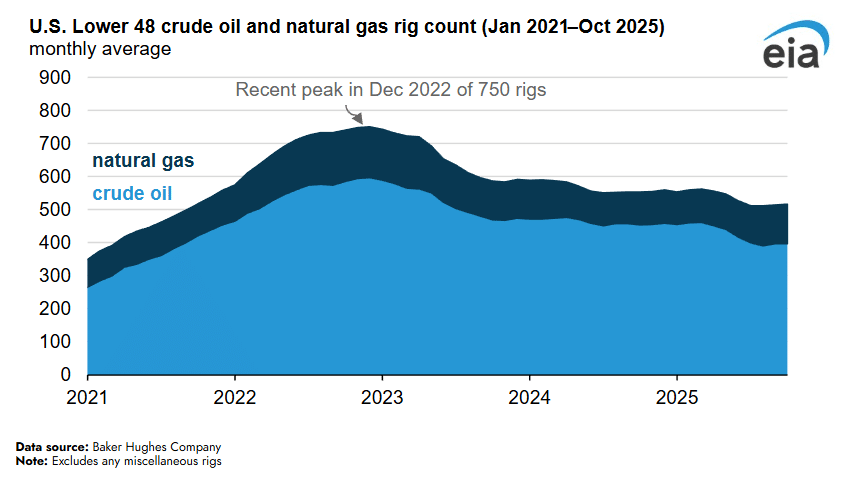

The US Energy Information Administration reports that the US oil and natural gas rig counts in the Lower 48 have steadily declined from 750 in December 2022 to 517 in October 2025, reflecting lower prices and improved drilling efficiencies. Oil-directed rigs fell 33% to 397, and natural gas rigs dropped 23% to 120, though both stabilized in October 2025.

Despite fewer rigs, production reached record highs, with crude oil at 11.4 million barrels per day in July 2025 and natural gas at 117.2 Bcf/d in August 2025, driven by more productive drilling techniques and longer lateral wells. The Permian and Appalachia regions saw production growth despite rig reductions. Looking ahead, 2026 forecasts predict a slight decline in crude oil (–1%) and a marginal increase in natural gas (<1%), with WTI prices expected to average $51 per barrel and Henry Hub natural gas at $4.02/MMBtu, influencing drilling activity. They write:

The average number of active rigs per month that are drilling for oil and natural gas in the U.S. Lower 48 states has declined steadily over the past few years from a recent peak of 750 rigs in December 2022 to 517 rigs this October. The declining rig count reflects operators’ responses to declining crude oil and natural gas prices and improvements in drilling efficiencies.

Since December 2022, the oil-directed rig count has dropped 33% to 397 rigs in October 2025, and the natural gas-directed rig count has declined 23% to 120 rigs over the same period. Natural gas-directed rigs dropped to 96 rigs in September last year amid historically low and prolonged natural gas prices. Both natural gas- and oil-directed rig count declines stabilized in October 2025.

The traditional link between rig activity and output has weakened recently, with production at record highs despite reduced rig counts. In July 2025, crude oil production in the Lower 48 set a monthly record of 11.4 million barrels per day (b/d), and in August 2025 natural gas production set a record of 117.2 billion cubic feet per day (Bcf/d). Operators have been focusing on the most productive plays, drilling longer lateral lengths to access more hydrocarbons, and using more efficient completion techniques to ensure economic viability.

The Permian region is the largest U.S. crude oil producing region and the largest contributor to U.S. crude oil production growth despite the total number of rigs dropping 29% since December 2022. Over this period, operators have increased oil production in the Permian by 18%, or 1.0 million b/d.

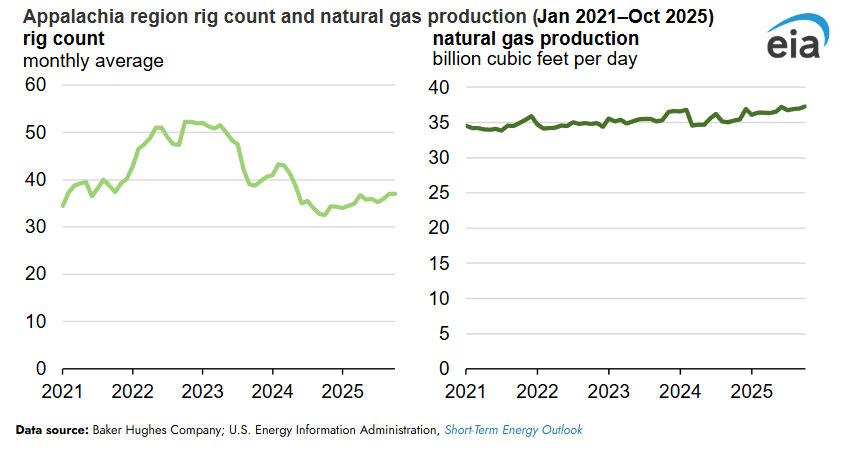

The largest U.S. natural gas producing region is Appalachia, where the total number of rigs dropped 29% while natural gas production increased 10% (3.3 Bcf/d) after stagnating in 2024 during a period of relatively low natural gas prices.

In our November Short-Term Energy Outlook, we forecast Lower 48 crude oil production in 2026 to decline slightly by 0.1 million barrels per day (1%) and natural gas production to increase by 0.4 Bcf/d (less than 1%). We expect the West Texas Intermediate (WTI) crude oil price to average $51 per barrel in 2026, 21% less than the 2025 average, and we expect the lower crude oil prices will limit oil-directed drilling activity. Conversely, we expect the Henry Hub natural gas price to rise to $4.02 per million British thermal units, 16% above the average for 2025. With these price shifts, we expect that increasing production from natural gas-directed drilling will more than offset decreases in natural gas produced as a byproduct of oil-directed drilling.