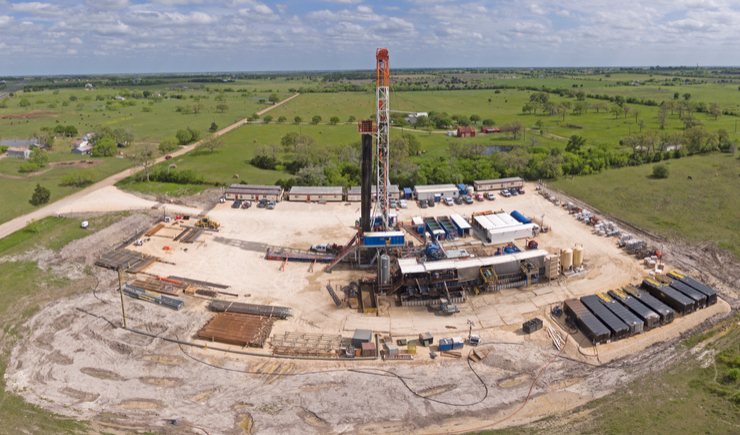

Despite soaring gasoline prices and ample oil in the ground in America’s shale basins, drillers won’t be able to save the country from the green agenda being pushed both by the Biden administration and ESG fund managers. Collin Eaton reports in The Wall Street Journal:

Shale companies are on track to spend a little more money pumping oil next year, but most aren’t opening up the spigots, even as prices top $80 a barrel.

Capital investments in U.S. oil patches this year are projected to come in at the lowest levels since 2004, years before the fracking boom made America the world’s top oil producer. Next year, oil companies are set to boost domestic spending 15% to 20%, analysts said. However, that will still be less than they plowed into drilling before the pandemic, and far less than the last time U.S. crude prices reached their current heights in 2014.

That’s because the pressure Wall Street put on American frackers to keep a lid on spending and oil production is still holding, analysts and executives said. Before the pandemic, whenever crude prices climbed to high levels, U.S. producers would flood the market with more barrels, but they ultimately spent more money than they made.

Investors and banks have now pressured oil companies to live within their means, pushing them to pay off debts run up during the shale boom and return extra cash to shareholders. They have also pressed companies to rethink future drilling plans and address their carbon footprints in response to environmental, social and governance, or ESG, concerns. Investors’ retreat from the sector has undercut the U.S. sector’s role as a reliable stopgap for global energy markets at a time when participants are worried oil supplies will tighten as demand recovers from the pandemic.

Read more here.