The US Energy Information Administration reports that in early 2023, the EU banned seaborne diesel imports from Russia, which had previously supplied half of Europe’s diesel, leading to a significant shift in global trade flows. Europe increased imports from the US and the Middle East, supported by new refinery capacity in Kuwait and Oman, while Russia redirected exports to countries like Brazil and Türkiye. In 2025, rising geopolitical tensions, including the Iran-Israel conflict and an attack on an Israeli refinery, further tightened supply and pushed up European gasoil crack spreads, an indicator of refinery profitability, which peaked in July before stabilizing in August as disruptions eased. They write:

In early 2023, the European Union implemented a ban on seaborne imports of diesel fuel, commonly called gasoil, from Russia following Russia’s full-scale invasion of Ukraine the previous year. The ban reoriented trade flows as Europe imported more diesel from the Middle East and the United States rather than Russia. This summer, Europe’s increased reliance on imports from the Middle East, coupled with conflict-related disruptions to refineries and escalating geopolitical tensions, contributed to a tightened global diesel market.

Before the ban, Russia supplied a significant portion of Europe’s diesel imports, accounting for 50% in 2022, according to data from Vortexa. The 2023 ban on diesel imports from Russia led to a rerouting of global trade flows of distillate. Distillate from Russia made its way to buyers such as Brazil and Türkiye, while importers in the rest of Europe needed new sources of distillate to backfill the lost volumes from Russia. In 2024, European distillate imports from Russia accounted for less than 1% of total seaborne imports from outside the region.

European imports of Russia’s distillate were replaced with increased imports of distillate from the United States and the Middle East. New refinery capacity in the Middle East, including the Al Zour refinery in Kuwait and the Duqm refinery in Oman, helped to supply the additional volumes of distillate to Europe. U.S. distillate exports shifted from Latin America to meet demand in Europe.

Earlier this year, escalating tensions related to Iran’s nuclear program led to rising geopolitical risks to petroleum supply chains from the Middle East to Europe. An attack on a 197,000-b/d refinery in Haifa, Israel, in mid-June led to significant tightening in Mediterranean refined product markets in the early summer.

Before the escalation, U.S. distillate exports were already high, but the four-week rolling average distillate fuel oil exports from the United States exceeded the five-year high for the seven consecutive weeks from May 9 through June 20, according to our Weekly Petroleum Status Report. Low supply from the Middle East led to draws on European inventories and rising refinery margins for distillate.

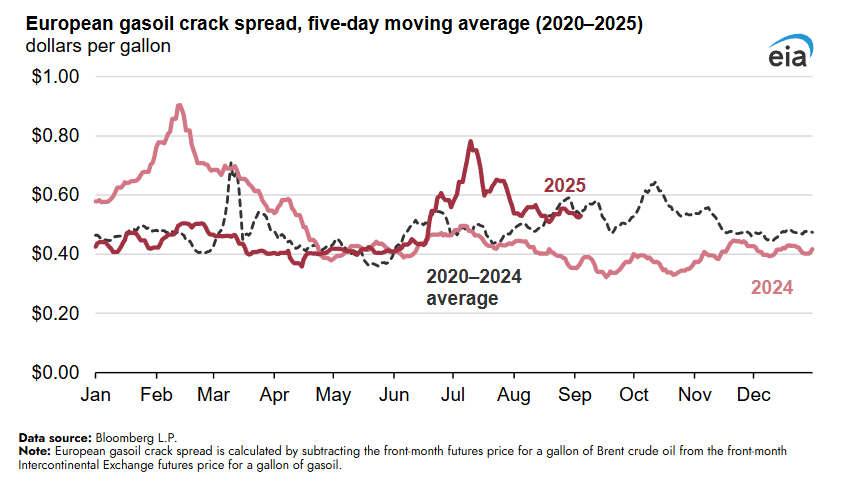

Rising gasoil crack spreads—a proxy for the profitability of refining gasoil—following conflict between Iran-Israel suggest market participants were concerned the conflict could limit Middle Eastern gasoil exports to Europe, which accounted for 43% of Europe’s gasoil imports in the first half of 2025.

The Intercontinental Exchange (ICE) gasoil crack spread calculated against Brent crude oil is one indicator of the relative value of gasoil in major European markets. The monthly average ICE gasoil crack spread increased 9 cents per gallon (gal), or 22%, in June and then an additional 15 cents/gal, or 29%, in July. The crack spread reached its highest point of the year at 84 cents/gal on July 10, before beginning to decrease. By mid-August, supply disruptions appeared to have been largely resolved, and the crack spread aligned with the 2020–24 average.