According to the Dallas Fed Energy Survey, US exploration and production firms report that average oil prices of about $43 per barrel are needed to cover operating costs for existing wells, while roughly $66 per barrel is required to profitably drill new wells.

Larger firms generally have lower cost thresholds than smaller operators. Despite higher oil prices, most companies plan to keep drilling activity steady in 2026, though some expect modest increases.

Firms remain optimistic about slight improvements in recovery rates and expect production growth to be led by the Permian Basin, while industry consolidation and geopolitical factors continue to shape outlooks. The Dallas Fed writes:

Exploration and production (E&P) firms

In the top two areas in which your firm is active: What West Texas Intermediate (WTI) oil price does your firm need to cover operating expenses for existing wells?

The average price across the entire sample is approximately $43 per barrel, up from $41 last year. Across regions, the average price necessary to cover operating expenses ranges from $34 to $47 per barrel. All respondents can cover operating expenses for existing wells at current prices.

Large firms (with crude oil production of 10,000 barrels per day or more as of fourth quarter 2025) require prices of $32 per barrel to cover operating expenses for existing wells, based on the average of company responses. That compares with $46 for small firms (fewer than 10,000 barrels per day).

In the top two areas in which your firm is active: What WTI oil price does your firm need to profitably drill a new well?

For the entire sample, firms require $66 per barrel on average to profitably drill, higher than the $65-per-barrel price when this question was asked in last year’s first-quarter survey. Across regions, average break-even prices to profitably drill range from $62 to $70 per barrel. Break-even prices in the Permian Basin average $67 per barrel, up from $65 last year.

Large firms (with crude oil production of 10,000 barrels per day or more as of fourth quarter 2025) require a $59-per-barrel price to profitably drill, based on the average of company responses. That compares with $68 for small firms (fewer than 10,000 barrels per day). The latest historical data can be found on the break-even page.

In light of the recent increase in oil prices, how has the number of wells your firm expects to drill in 2026 changed since the start of the year?

This question was posed only to E&P executives who each said their firms drilled or completed horizontal wells in the past two years. Half of the executives surveyed said the number of wells their firms expect to drill in 2026 has not changed since the start of the year. Twenty-six percent said they expect the number of wells they drill to “increase slightly,” and 21 percent said it would “increase significantly.” Conversely, 3 percent said drilling expectations “decreased significantly.”

Executives at small E&P firms were more likely than their counterparts at large firms to indicate they increased the number of wells they plan to drill since the beginning of the year. In the U.S., small E&P firms are greater in number, but large E&P firms represent the majority of production (more than 80 percent). A breakdown of the data is shown below.

Response

Percent of respondents (among each group)

All E&P

Large E&P

Small E&P

Increase significantly

21

8

29

Increase slightly

26

23

29

Remain the same

50

69

38

Decrease slightly

0

0

0

Decrease significantly

3

0

5

NOTES: Executives from 34 exploration and production (E&P) firms answered this question during the survey collection period, March 11–19, 2026. Small E&P firms produced fewer than 10,000 barrels per day (b/d) in fourth quarter 2025, while large E&P firms produced 10,000 b/d or more. Responses came from 21 small firms and 13 large firms. This question was posed only to executives who each said their firm drilled or completed a horizontal well in the past two years.

SOURCE: Federal Reserve Bank of Dallas.

All firms

There remain about 30 publicly listed independent exploration and production (E&P) firms in the U.S. with market capitalizations of over $1 billion each. How many such firms do you think will remain by the end of this decade?

The most selected response was “19–24” (47 percent of respondents), followed by “13–18” (26 percent) and “≥25” (17 percent). A smaller percentage selected “7–12” and “0–6.”

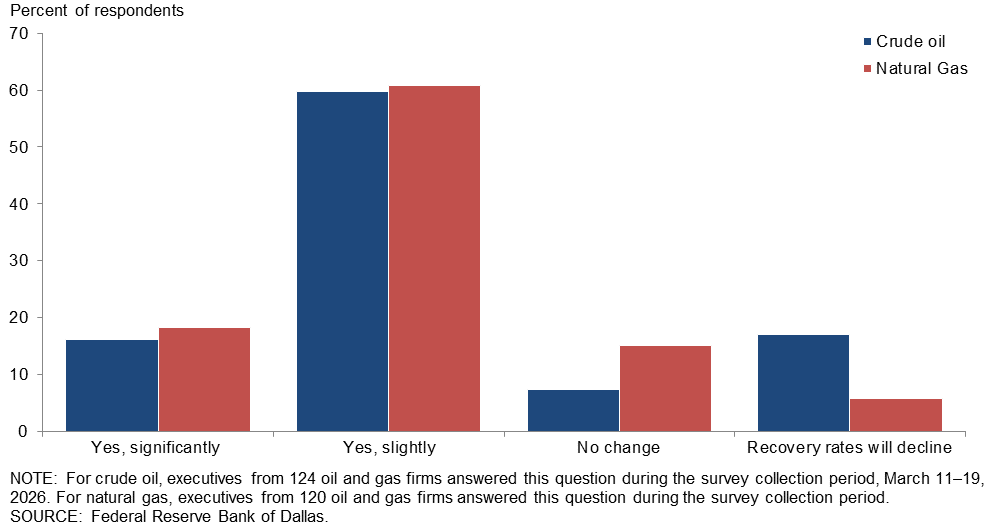

Do you expect upstream firms will be able to increase oil recovery rates from U.S. shale wells over the next 10 years? How about for natural gas?

Firms generally expect recovery rates to increase over the next 10 years. For both crude oil and natural gas, the most selected response was “yes, slightly.” Firms were slightly more optimistic about improving recovery rates for natural gas than crude oil.

In which basins or regions do you expect U.S. oil production to increase from December 2025 to December 2026? (Check all that apply.)

Respondents could choose more than one answer for this special question. The most selected response was “Permian” (82 percent of respondents), with “Eagle Ford” and “Utica (Ohio)” each selected by 29 percent of respondents.

How have your expectations changed for Venezuelan oil production over the next 24 months when compared with your expectations three months ago?

The largest group, 55 percent of executives, expect slightly more Venezuelan oil production over the next 24 months when compared to expectations three months ago. Twenty-nine percent of executives have not changed their expectations, while 12 percent expect significantly more production. A smaller percentage expect either slightly less or significantly less production from Venezuela.