Originally posted December 5, 2022.

The ISM Manufacturing index fell into contraction territory in November for the first time since 2020. The ISM index is a monthly survey of purchasing managers at more than 300 manufacturing firms. The index measures the change in manufacturing activity from month to month. Activity in housing, a large cyclical sector of the economy, has also turned down, and homebuilder sentiment is at recessionary levels. We are also seeing some weakness in advertising markets and softness in other sectors of the economy.

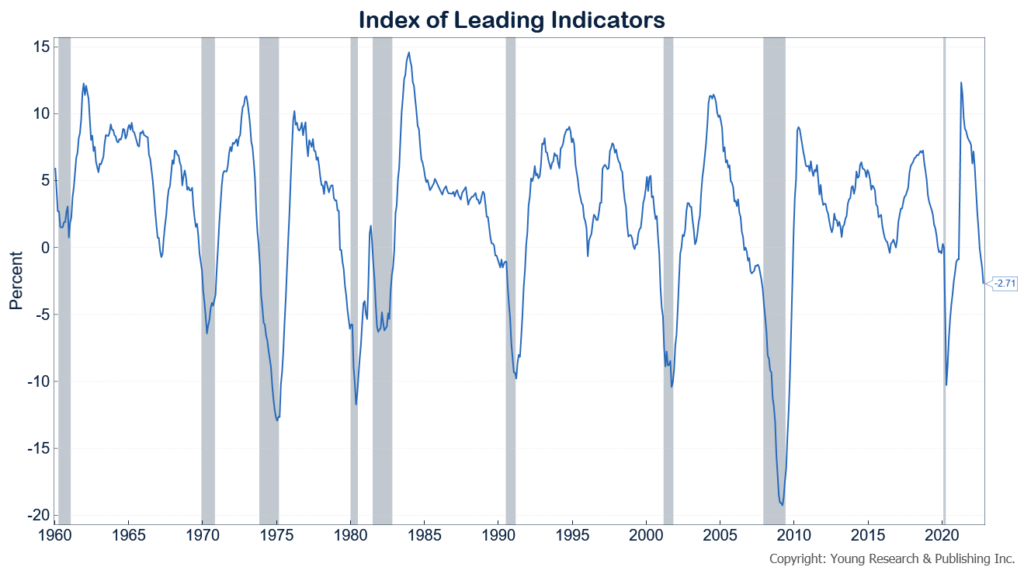

The leading economic indicators which seek to provide an early warning sign of recession have a foul look. On a year-to-year change basis, the leaders are clearly pointing to recession.

Based on the unrevised data we have in hand, the odds likely favor recession in the coming 6-12 months, but that is not yet a guarantee. What’s more, recession means little without considering severity.

The jobs market remains solid, with wage growth strong, unemployment near historic lows, and new job creation far in excess of the number of jobs needed to keep up with population growth. There are also still trillions in excess savings that consumers can tap into in order to soften the blow of an economic downturn.

Consumer spending accounts for 70% of the economy. A solid jobs market and healthy consumer balance sheets may mean that the severity of recession, should one be realized, may be on the mild side.