Is it true that the Fed holds over $8 trillion in assets on its balance sheet and that it has created 4 trillion dollars out of thin air since the pandemic began?

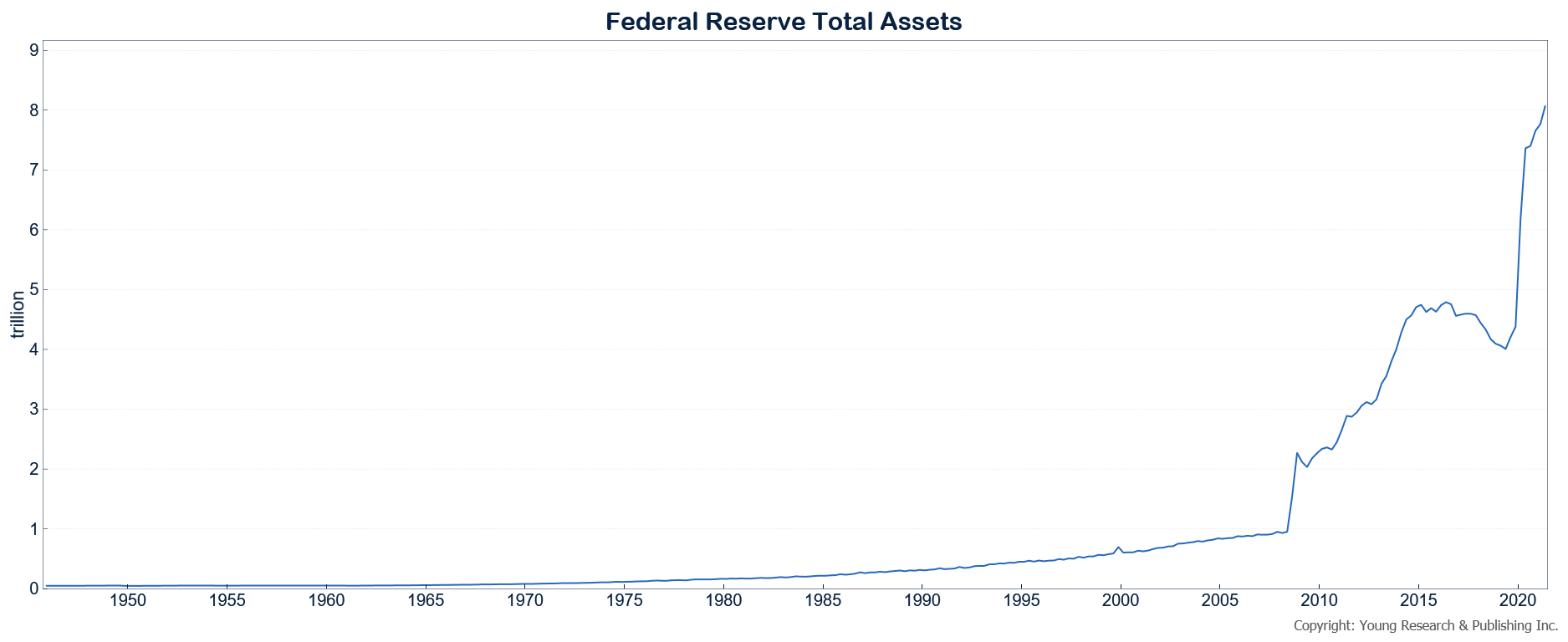

Indeed it is. At the end of February 2020, the Fed held just over $4 trillion in assets. As of today, the Fed’s balance sheet stands at $8.2 trillion. Three-quarters of that increase, or $3 trillion, was created over a period of about 12 weeks last year.

Four trillion dollars is a lot of money. That’s more than the total revenue the Federal government collects in a year. Did Congress pass a law last year that allowed the Fed to create $4 trillion?

Nope, Congress gave the Fed the authority to expand and contract the size of its balance sheet at will without pre-approval decades ago.

Wasn’t the Fed created to lend money to banks in a panic?

The Fed was created in 1913 to provide liquidity to the banking system in a panic. That was before federal deposit insurance from the FDIC. In 1978, Congress expanded the Federal Reserve’s mandate.

Today, the Fed’s mandate reads:

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long-run growth of the monetary and credit aggregates commensurate with the economy’s long-run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.”

This is the dual mandate the Fed often refers to when it tries to justify its policy actions, but if you read the text of the mandate, it has three components. To 1) promote maximum employment, 2) keep prices stable, and 3) maintain moderate long-term interest rates.

Why don’t we ever hear about the third part of the mandate? Aren’t savers and retired investors hurt the most by today’s extremely low interest rates? Doesn’t moderate mean average or not extreme?

It would certainly help savers and retired investors if the Fed paid attention to the third part of its mandate.

Has the Fed always used its balance sheet to meet its congressional mandate?

The chart below shows the Fed’s total assets since 1945. The Fed’s total assets increased at a fairly steady rate as the demand for currency in circulation rose. The Fed’s balance sheet was a non-factor for decades.

It wasn’t until 2008, when Chairman Ben Bernanke decided to spearhead the greatest bailout and financial intervention in American history, that the Fed’s balance sheet exploded.

During the height of the panic in 2008 and 2009, the Fed started to expand its balance sheet by electronically printing money to help facilitate liquidity in the financial system. The initial burst of money printing totaled about $1 trillion and could have been wound down soon after the panic subsided.

Unfortunately, the Fed decided the expanded powers it had used to prevent a panic would become part of its regular monetary policy tool kit. Over the ensuing five years, the Fed printed an additional $3 trillion to buy Treasury and Mortgage bonds.

Financial markets love the Fed’s bond buying. It decreases the float of bonds, pulls down long-term interest rates, and pushes investors into riskier assets.

During this era of extreme monetary policy intervention, when the Fed began its bond-buying program, bond yields plummeted, and valuation ratios on stocks soared. The Fed has taken risk out of the market. Speculators, traders, and any and all in between are allowed to succeed, but at the first sign of turbulence, the Fed comes to the rescue.

This theme was repeated during COVID. Not to be outdone by Chairman Bernanke, Jay Powell, pushed the Fed deeper into the game of babysitting speculators and traders.

While it took Bernanke seven years to print $4 trillion, Jay Powell did it in 17 months, and he took it a step further by forever changing the corporate bond market.

By bailing out investors in the corporate bond market, the Fed has signaled to all market participants that it will come to the rescue in all future downturns. It doesn’t matter that the Fed was not permitted to purchase corporate bonds. Powell & Co. used financial engineering to get around the limits of the Federal Reserve Act. You can be almost certain investment-grade corporate bonds, and high-yield bonds will be purchased during the next recession. There is even a chance the Fed would use financial engineering to purchase stocks and claim the interventions are risk-free.

How has the Fed’s extreme use of its balance sheet and ultra-low interest rates changed the economy and the financial system?

Starting under Chairman Bernanke, the Fed has made a mockery of the free enterprise system that has helped America become the wealthiest nation on earth.

The era of QE has created massive mispricing and misallocation across the economy and financial markets. The benefits of capitalism are lost when you bail out speculators, the imprudent, and the reckless.

Populism is on the rise, partly because the biggest beneficiaries of the Fed’s largesse are leveraged hedge funds and others who least need the help. The conservative retiree who wants simply to generate a safe and secure retirement income has no good options today. Treasury bonds yield almost nothing after adjusting for inflation.

The stock market may offer more upside, but it also comes with major risks after more than a decade of inflating asset valuations and falling yields.

And when over $4 trillion dollars can be created over the course of a year with the click of a button, the U.S. dollar looks like a currency destined for an eventual demise.