One of the major factors that will impact the outlook of the Vanguard GNMA fund in 2017 is the Federal Reserve. After holding rates near zero for almost a decade, the Fed finally began a process of normalizing interest rates. The Fed has explained to the public it plans to raise interest rates at a gradual pace until the overnight interest rate is at a level that neither stimulates nor restrains economic growth.

Compared to prior cycles, the Fed’s normalization of interest rates has been more glacial than gradual, with only three rate hikes in the 17-month period. But with inflation and unemployment now near the Fed’s targets, the pace of interest rate hikes is likely to accelerate.

How will GNMA securities perform in an environment where the Fed is hiking interest rates at a faster pace? And what about the Fed’s balance sheet?

A faster pace of interest rate hikes isn’t the only thing Vanguard GNMA investors have to worry about in 2017. The Fed has also signaled that it plans to wind down the trillions worth of mortgage securities on its balance sheet later this year or early next year.

How will GNMA bonds perform in this environment?

Outlook for GNMA Bonds

To get a good handle on the outlook for GNMA securities it is important to understanding the factors that drive their returns.

GNMA securities are mortgage-backed securities. Mortgage-backed securities are bonds backed by payments on mortgage loans. The loans are pooled and then out of those pools securities are issued that entitle holders to a share of interest and principal. GNMA’s are the only mortgage-backed securities that are explicitly backed by the full-faith and credit pledge of the United States government.

GNMA Securities vs. Conventional Bonds

Mortgage-backed securities are not like conventional bonds. Conventional bonds pay interest during the life of the bond and all principal at maturity. Mortgages pay principal and interest every month in varying amounts. Most investors intuitively understand this. When you take out a mortgage, you make a payment each month that includes interest and principal. When you refinance your mortgage, you are making what is called a pre-payment.

Pre-Payment Risk

Because GNMA securities are backed by the U.S. government, they are free of credit risk, but they do carry pre-payment risk and extension risk. Pre-payment risk is the risk that your principal will be repaid before maturity. Why is getting paid early a risk?

Let’s say you invest in a GNMA security and every mortgage backing that security has a 6% rate. Fast-forward one year and assume that mortgage rates have fallen to 4%. Further assume that every mortgage backing the GNMA security is refinanced to lock in that lower 4% rate. As the investor in this GNMA security, the entire balance of your principal is returned to you. You can reinvest in another GNMA security, but the prevailing rate on GNMA securities is now only 4%. Instead of earning 6% on your money, you now earn 4%.

Extension Risk

Extension risk is the opposite of pre-payment risk. When interest rates rise, the rate of pre-payments on GNMA securities slows, which effectively extends the maturity of a GNMA security. You now have a longer maturity bond than you originally invested in just as interest rates are rising. The combination of higher rates and a longer maturity results in a lower price.

While interest rates are the big factor that determines the percentage of a pool of mortgage backed securities that is paid back ahead of maturity, it is not the only factor. The rate of pre-payments on a pool of mortgages also depends on the historical path of interest rates, housing turnover, the aging of loans, seasonality, and credit conditions among other factors.

In return for taking on pre-payment risk and extension risk, investors in GNMA securities are compensated with yields that are greater than the yields on Treasury securities. How much greater varies over time and by measurement.

The Factors that Influence Risk

Some of the major factors that influence pre-payment risk and extension risk include the level of interest rates, the historical path of interest rates, housing turnover, the aging of loans, seasonality, and consumer credit conditions. I’ll focus on a few of these factors.

With the Fed hiking interest rates and talking about winding down its mortgage securities holding, the risk GNMA investors should be focused on today is extension risk.

After a prolonged period of low interest rates where many homeowners have refinanced, an increase in long-term interest rates is likely to result in fewer refinancings. This will extend the average maturity of GNMA securities at the same time that interest rates are rising. Neither factor is bullish for GNMAs.

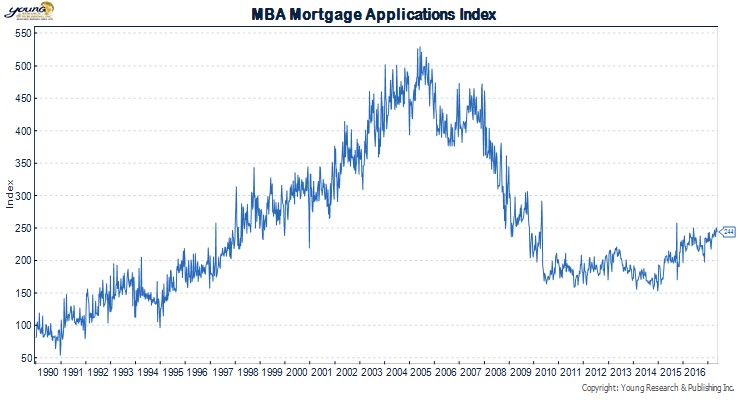

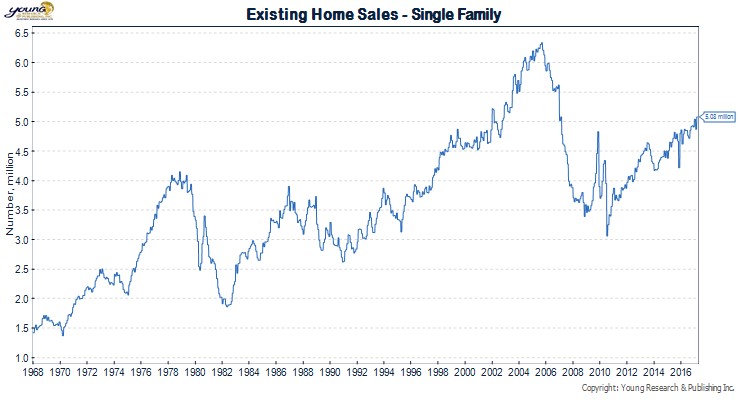

The upshot is that housing turnover has likely not yet peaked for the cycle. The number of mortgage purchase applications is still depressed and existing home sales has more of a mid-cycle look. (See charts below).

Greater housing turnover could cushion the blow that GNMA securities will feel should longer-term interest rates increase.

I say should, because it is not a given that an increase in the short-term interest rates the Fed controls will result in an increase in the long-term interest rates most relevant for GNMA investors.

Since the Fed first hiked short-term interest rates in December of 2015, long-term interest rates are essentially unchanged. Bond buying programs by the European Central Bank as well as the Bank of Japan are likely having an impact here, but there is also a valid case to be made that rates haven’t risen because investors are seeing more signs of late-cycle behavior in the economy.

What about the unwinding of the Fed’s holdings in mortgage backed securities? Will the Fed getting rid of its mortgage bonds push up interest rates on GNMA bonds? It could, but the Fed recognizes that it is a big player in the mortgage bond market and it is likely to move slowly and cautiously. The last thing the Fed wants to do is disrupt the housing market by spiking mortgage rates.

That’s not to say it won’t or can’t happen, but we would expect to see some backtracking if such a scenario unfolded.

The Bottom Line on Vanguard GNMA

The extension risk in GNMA securities may be higher today than it has been in some time, but that doesn’t mean GNMA securities are a poor investment. Every investment carries some risk. The question investors must answer is, am I being fairly compensated for that risk? At a current yield of 2.65% (Merrill Lynch GNMA index yield) are investors getting a fair shake?

We think so and we think Vanguard GNMA should play an important role in a diversified fixed income portfolio.