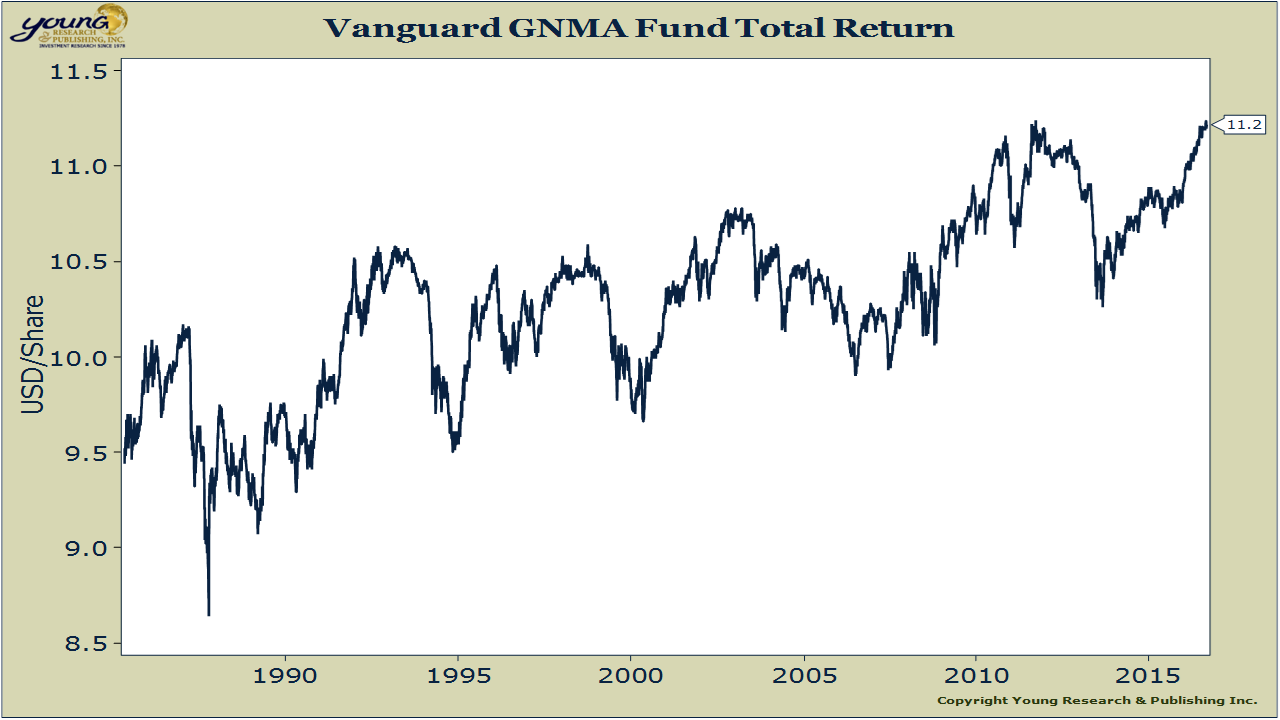

What should you do about Vanguard GNMA? Let’s change the question. What should you do about your house or an investment property when there’s a change in price? Answer: not much. “Think about your GNMA fund as you would a piece of income property. For a landlord, it’s a waste of time to worry about the price you could get for the property from month to month. The monthly rents are what pay the bills. GNMA is your triple-decker. Why sell it? You need the rent money.”

I wrote that to you back in March of 2013. And guess what GNMA did? Well, it took a nose dive of course. Sorry. Yup, it kept on going down, down, down, down for another four months. Not fun. But if you stuck around, you were able to pick up more shares for less money. Since GNMA hit bottom in September of 2013, shares are up over 9.3%.

Looking back or looking forward, I don’t get too excited about the ups and downs. Why? Because I like them both—the ups and the downs. In a perfect world the market will be on a steady decline—as you squirrel your money away—right up until the day you retire. See ya boss! Then it jumps by a thousand percent on day one of retirement. You’re golden! Why not take advantage of the times when you’re investing/re-investing when prices are down? What you’ll find is that, over time, even the blind squirrel finds a nut.