At the Cato Institute, Scott Lincicome explains that the panicked outcry over the “retail apocalypse” is overdone and that, in fact, retail isn’t dying but changing. He writes:

Among the more common economic tropes of the last 15 years has been the U.S. “retail apocalypse.” Giant e‑commerce companies, so the story goes, have killed traditional brick-and-mortar establishments in the United States, forcing American shoppers—particularly low-income ones—to travel farther for fewer (and lesser) retail opportunities and leaving them worse off overall. Communities have, in turn, supposedly suffered from a loss of jobs and tax revenue, as well as a blight of empty storefronts and shopping malls. And, thanks to pandemic-era lockdowns, it’s only gotten worse in recent years.

Fears of the retail apocalypse have fueled not only piles of breathless reporting on certain store closures and their national economic implications, but also government policy, as states and localities across the United States have responded with subsidies for local businesses, new taxes on online sales, bans on “big box” stores, and so on. Yet, even a decade ago, there were clear signs that the “retail apocalypse” wasn’t actually happening—that brick-and-mortar retail was changing, not dying, and that Americans were basically fine with the result. Now comes a great new paper from the National Bureau of Economic Research (NBER) confirming the early pushback and strongly cautioning against efforts to regulate American retail businesses now or in the future.

The Retail Apocalypse Never Actually Happened

Economist Yue Cao and colleagues tested the retail apocalypse thesis by first examining changes in general merchandise stores—25 different national chains and several smaller regional outlets—in 18 metro areas between 2010 and 2019. Then, using these figures and smartphone geolocation data for more than 2.7 million devices, they estimate whether Americans in these places were better or worse off (in terms of “consumer surplus”) in 2019 than they were 10 years earlier.

They found, first and contrary to the conventional wisdom, the number of general merchandise stores in the United States actually increased in the 2010s, from 49,089 to 52,807, as dollar stores, supercenters, and discount department stores more than replaced certain traditional department stores and regional chains.

Second, Americans’ access (defined as having a store within 10 miles) and proximity to the retail chains examined also improved from 2010 to 2019, with dollar stores again being a big driver of the improvement but also gains—dots on the left side of the line in the chart below—at Target, Walmart, and my personal favorite, Costco.

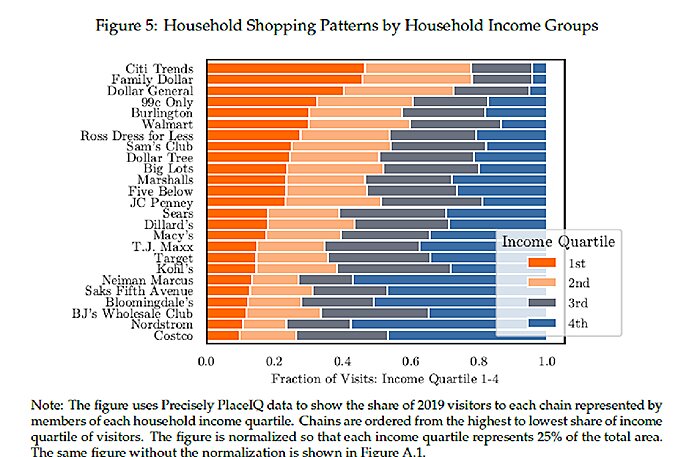

As you’d expect, Americans’ choice of retail establishment differed greatly according to their incomes, with this difference driven by both consumers’ preferences and the stores’ locations. Among the most “egalitarian” (meaning a roughly equal share of store visits by rich, poor, and middle income) stores were Ross, Sam’s Club, Marshalls, and Five Below (which my daughter loves, btw):

Next the authors examined Americans’ preferences for various retail establishments, measured by their willingness to drive to a certain store in their general vicinity. (If you’re willing to drive a few extra miles for similar stuff, you very likely prefer the place selling it.) Here, they found that Walmart was the most preferred general merchandise store among both low-income and high- income Americans, while everyone basically hated traditional department stores. (And, seriously, who can blame them?) Other consumer preferences were pretty much what you’d expect, with lower-income consumers preferring discount chains and wealthier ones frequenting warehouse clubs and higher-end department stores like Nordstrom. And others still were weird/surprising (e.g., wealthier people preferred Dollar Tree over other dollar stores).