The economy may be growing slowly or even shrinking somewhat, but the time for radical monetary policy is long since over.

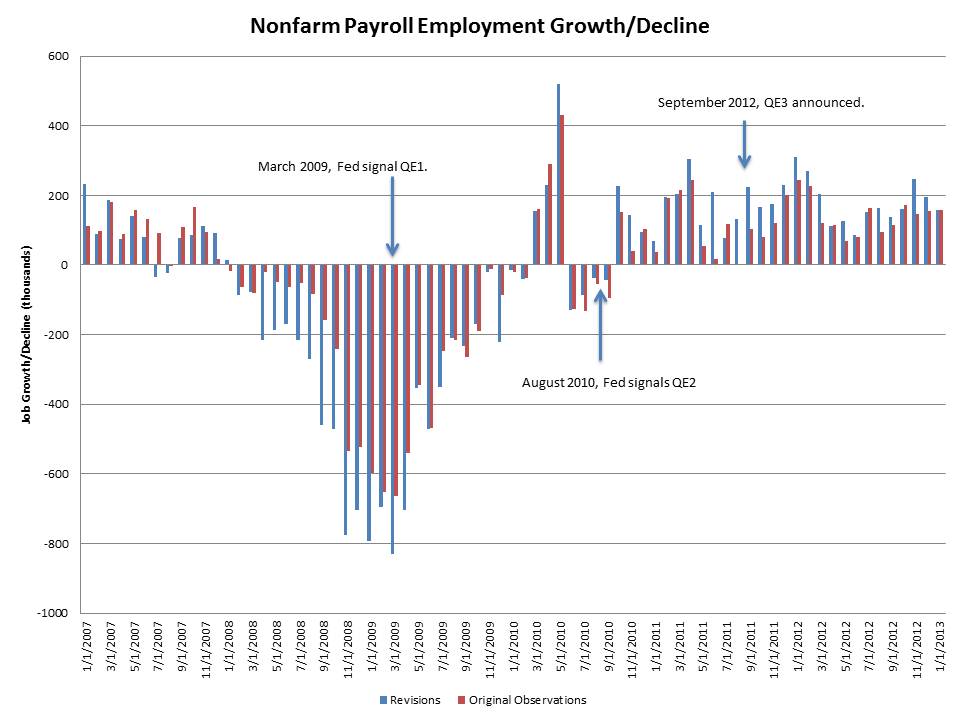

Revisions in today’s employment report outlines clearly that the Fed is overreaching. In the last two months, those the Fed was looking at during its latest policy meeting, employment growth was revised significantly upward. The number of new jobs created in December increased from 155,000 to 196,000, and November’s total was revised from 161,000 to 247,000. These aren’t roaring numbers, but they certainly don’t call for emergency monetary policy.

In fact, employment has been better than it was reported for quite some time. In the thirty months since the Fed announced QE2, 26 have had payroll employment revised upward. That is one among many of the flaws of using monetary policy to target inflation. Every time the Fed was using weak initial employment data to justify its no-holds-barred monetary stimulus, the numbers were better than initially reported. Once revisions are factored in, growth in employment since August 2010 has been 160,000 per month. Since the Fed announced QE3 in September, average employment growth after revisions has been 180,000. In the last three months, average employment growth has been 200,000.

The Fed has communicated that it will consider altering its monetary policy after six months in a row of 200,000 job growth. But the time to abandon such policies has long since passed, and every day the Fed waits to turn the ship around is one more day it is headed toward the rocks of inflation.