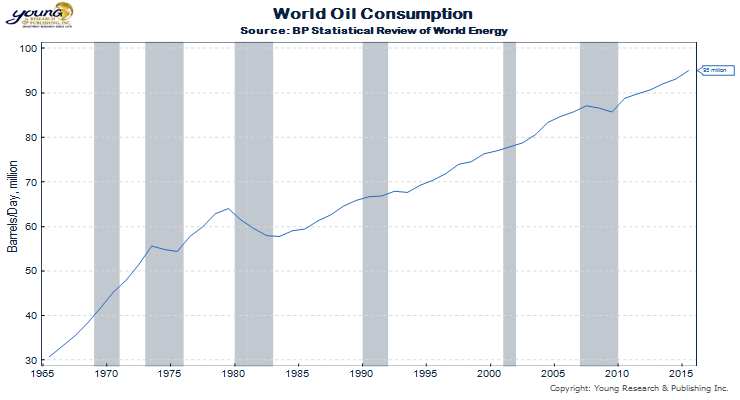

You can see on my chart that, aside form a couple hiccups, consumption of oil has been rising without much difficulty since the early 1980s.

The big declines in oil consumption you can see on the chart are all recession driven (the shaded areas represent periods of economic recession in the United States). But according to the Wall Street Journal’s Lynn Cook and Elena Cherney, that may be about to change.

While most big oil companies foresee a day when the world will need less crude, timing when that peak in oil demand will materialize is one of the hottest flashpoints for controversy within the industry. It’s tough to predict because changes to oil demand will hinge on future disruptive technologies, such as batteries in electric cars that will allow drivers to travel for hundreds of miles on a single charge.

Hitting such a plateau would mark the first time that demand has declined even when economies are growing since Col. Edwin Drake jury-rigged a pipe to drill for oil in Pennsylvania in the late 1850s. Yet, for many companies and investors, the question isn’t whether this immense turning point will happen—it’s when.

Getting that timing right will separate the winners from the losers, and it has become a major preoccupation for energy economists and a flashpoint for controversy within the industry.

Forecasts for peak oil demand diverge by decades. The Paris-based International Energy Agency argues that demand will grow, albeit slowly, past 2040. And the two biggest U.S. oil companies, Exxon MobilCorp. and ChevronCorp., say peak demand isn’t in sight.

But some big European producers predict that a peak could emerge as soon as 2025 or 2030, and they are overhauling their long-term investment plans to diversify away from crude oil.

Read more here.

Saudi Aramco CEO Amin Nasser poured cold water on the idea of “peak oil demand” when asked about it by Bloomberg in April.

“The global economy is forecast to double in size by 2050” so overall demand for energy will be higher, Saudi Arabian Oil Co. Chief Executive Officer Amin Nasser said at the International Oil Summit in Paris. The idea that oil demand is close to its maximum level is “equally as misleading” as now-discredited theories about peak oil supply, he said.

McKinsey & Company offers a view that might not be apparent when thinking topically about oil demand. McKinsey factors in the growth of demand for petrochemicals, i.e. plastics, especially in developing markets. But even with growth in demand for plastics, oil could see a reduction in overall demand if recycling picks up a bit.

Energy outlook: Key insights

Our business-as-usual case integrates the latest McKinsey view on economic-growth fundamentals and granular sector and regional insights. Six key points have emerged:

- Growth in global energy demand will decelerate to 0.7 percent per year through 2050, a rate 30 percent slower than we had previously forecast.

- Emerging and developing countries1will drive all growth in energy demand, while European and North American demand will decline.

- Chemicals will grow at more than double the rate of total energy demand, while light-vehicle demand will peak around 2023.

- Demand for electricity will outpace demand for other energy sources by more than two to one. Solar and wind will represent almost 80 percent of net added capacity and 34 percent of generation by 2050.

- Fossil fuels will dominate the total energy mix through 2050, but their share of total energy will decline to 74 percent from 82 percent. While gas is a relative winner (growing at almost twice the rate of total energy demand), coal will peak by 2025, and oil demand growth will flatten to 0.4 percent.

- Energy-related carbon dioxide emissions will flatten and start to decline around 2035 as a result of the transformation of light vehicles (more-efficient combustion engines and more electric vehicles on the roads) and the strong shift to wind and solar in power generation.

Could peak oil demand be in sight?

The total demand for liquid hydrocarbons will play out as a tug of war between growth in the petrochemical sector and declining demand from passenger cars. Petrochemical feedstock will drive 70 percent of the growth in demand for liquid hydrocarbons through 2035. Demand for liquids, excluding chemicals, will peak and flatten by 2025 because of a decline in demand from light vehicles. The petrochemicals demand will drive the growth of light end products, a large share of which are not made from crude oil.

Petrochemicals. The industry’s traditional rule of thumb is that chemicals demand grows at 1.3 to 1.4 times the rate of GDP. Globally, we see this relationship changing, especially as mature markets reach a saturation point for plastics. Markets such as Germany and Japan are clearly declining in per capita plastics demand. As a result, we see chemicals demand growing at only 1.2 times GDP in the short term, from a global perspective. In the long term, that growth will decline to match the GDP growth rate. Two elements could transform chemicals demand further: plastics recycling and plastic-packaging efficiency. If we imagine that global plastic recycling improves from today’s 8 percent rate to 20 percent in 2035 and that plastic packaging use declines by 5 percent, demand for liquid hydrocarbons driven by chemicals could be approximately 2.5 million barrels per day below our business-as-usual case.

Read more here.