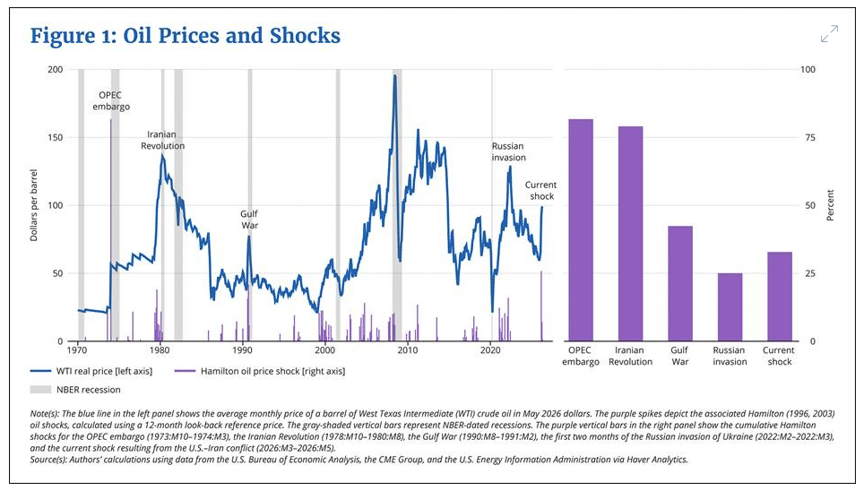

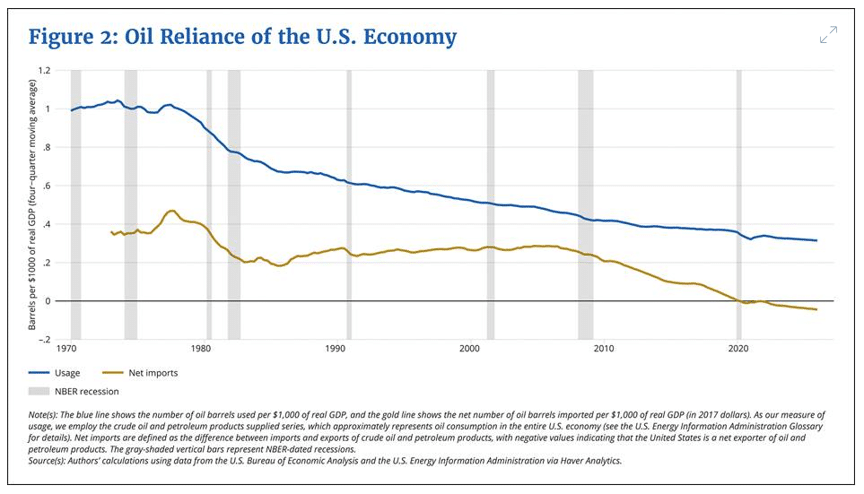

A Federal Reserve Bank of Boston paper, “Reassessing the US Economy’s Vulnerability to Oil Shocks,” argues that the United States is much less vulnerable to oil-price spikes than it was during the 1970s. The paper explains that the economy now uses less oil relative to its size, and increased domestic production—especially from shale oil—has reduced dependence on foreign energy sources. As a result, oil shocks have a smaller impact on overall economic activity.

The Boston Fed finds that rising oil prices still contribute to inflation, but their effect is weaker than in the past because energy accounts for a smaller share of household and business spending. While inflation remains sensitive to large oil-price increases, the broader economic consequences are less severe than they once were.

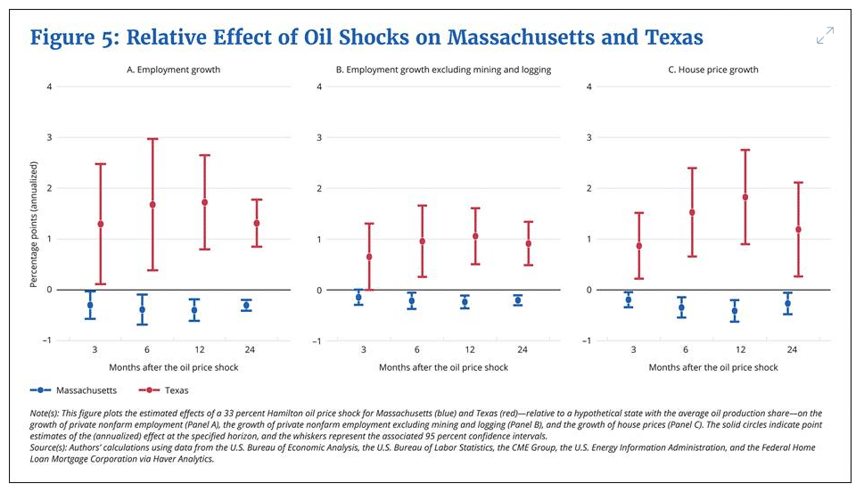

They also show that oil shocks now have a much smaller effect on employment. Higher oil prices can benefit energy-producing states, helping offset losses in other regions. Consequently, oil-price spikes are more likely to create inflationary pressures than widespread job losses.

The paper concludes that modern oil shocks present a different challenge for policymakers. Since employment appears more resilient while inflation still rises, the Federal Reserve may be able to focus more on controlling inflation without facing the same unemployment concerns that characterized the oil crises of the 1970s.