Global natural gas markets have split sharply following the closure of the Strait of Hormuz, with prices rising in Europe and Asia while declining in the United States. European benchmark TTF and Asia’s JKM climbed 35% and 51%, respectively, whereas US Henry Hub prices fell amid strong domestic supply and limited capacity to boost exports.

The disruption has taken roughly 20% of global LNG supply offline—primarily from Qatar—forcing buyers in Europe and Asia to compete for alternative shipments and driving prices higher, according to the US Energy Information Administration. Although US exports may edge up, terminals are already running near full capacity, limiting their ability to fill the gap.

The result is a widening global price divide, underscoring growing regional imbalances in natural gas supply and demand. The EIA writes:

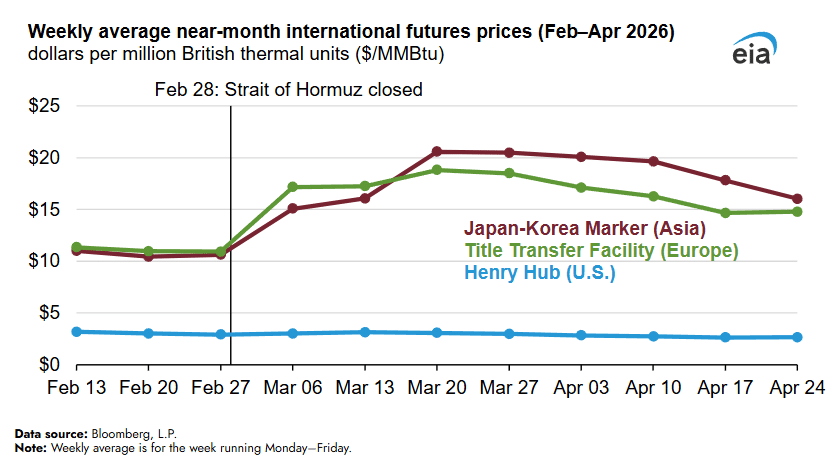

Prices for natural gas in Europe and Asia have diverged from those in the United States since the February 28 closure of the Strait of Hormuz.

Futures prices for liquified natural gas (LNG) delivery to the Title Transfer Facility (TTF), the European benchmark price, increased to $14.80 per million British thermal units (MMBtu) for the week ending April 24, 35% higher than before the closure, according to data from Bloomberg L.P. In East Asia, the front-month futures price for the benchmark Japan-Korea Marker (JKM), rose 51% over the same period to $16.02/MMBtu. In contrast, natural gas prices at the U.S. benchmark Henry Hub have decreased 9% since February 28 due to limited opportunities for increasing LNG exports in the near term and ample domestic seasonal natural gas storage and supply.

The closure of the strait has affected over 10 billion cubic feet per day (Bcf/d) of global LNG supplies, or approximately 20%, mostly from Qatar’s Ras Laffan export facility. No laden LNG vessels are known to have crossed the strait between March 1 and April 24, according to Kpler data.

We expect U.S. LNG exports will increase, but only by a small portion of the missing volumes. Since the closure, the U.S. Department of Energy has approved two increases to terminal export authorizations to countries lacking free trade agreements (FTAs) with the United States since February—Plaquemines LNG (0.5 Bcf/d) in March and Elba Island (0.1 Bcf/d) in April. Countries lacking FTAs are the destinations for almost all U.S. LNG export volumes. In addition, we expect that approximately 2.4 Bcf/d of DOE-authorized export capacity will come online between April and December 2026—Golden Pass (Trains 1–2) and Corpus Christi Stage 3 (Trains 5–7).

Operators already run U.S. LNG terminals at high utilization rates, limiting additional natural gas export growth, which in turn limits the potential for significant price increases in the U.S. domestic market. The United States exported an estimated 17.9 Bcf/d of LNG in March, the second-highest monthly export volume since December 2025’s record 18.4 Bcf/d. The export terminal capacity utilization in March amounted to 94% of the maximum DOE-approved export levels, according to our most recent Short-Term Energy Outlook and Liquefaction Capacity File. Exports rose from an estimated 17.3 Bcf/d in February, with a 91% terminal utilization rate.

QatarEnergy declared force majeure on March 4, which has forced Asian buyers who import over 80% of Qatari gas to compete for spot cargoes on global markets to replace lost contract volumes. Although average weekly TTF prices have fallen from a three-year high reached in mid-March, prices remain elevated compared with February. European natural gas storage inventories finished the winter season at 28% full, below the five-year average of 41%, according to Gas Infrastructure Europe, which will likely require more spot cargoes to refill storage inventories prior to next winter. Asian natural gas storage capacity is less than European capacity, and JKM prices are likely to move with weather-related spot demand.

The weekly average front-month futures prices for the U.S. benchmark Henry Hub have remained generally insulated from price volatility abroad. Henry Hub futures prices have fallen 9% since the week ending February 27 as the winter season ends and domestic consumption has declined. At the beginning of injection season, daily Henry Hub prices for the prompt-month were the lowest since October 2024.