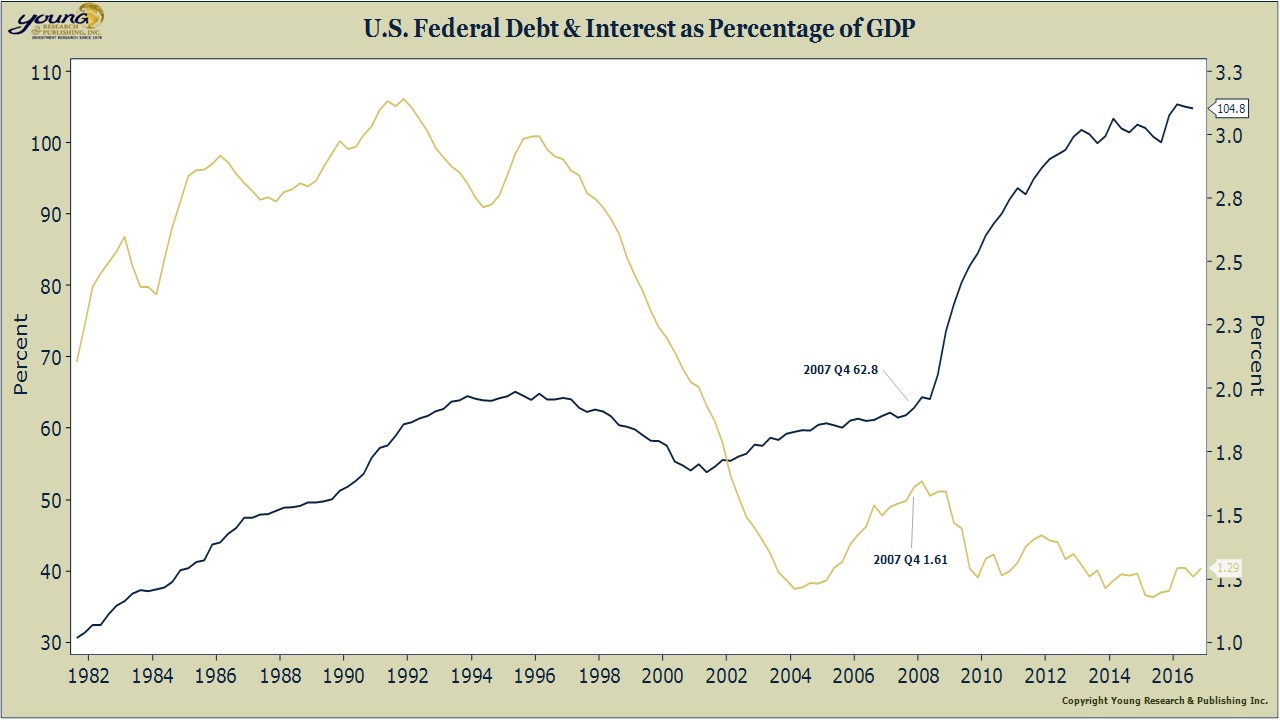

Over the last eight years, the federal government has been on an unprecedented spending spree. Since year-end 2007, federal debt outstanding has increased by more than $10 trillion—a number so large it is hard to even wrap your mind around. But let’s try.

According to the Census Bureau there are almost 125.8 million households in the United States. The $10 trillion increase in federal debt equates to almost $80,000 per household.

Do you and your family feel like you’ve gotten $80,000 worth of value from the government over the last eight years?

For $10 Trillion, the U.S. government could have purchased every publicly traded company in the euro-area.

It could have retired all state and local government debt plus all of America’s consumer debt and still had a couple trillion left over.

It could have retired 70% of all outstanding mortgage debt in America.

You get the point. A ton of money was spent, and in the eyes of many Americans, it was darn near a complete waste. But that’s not even the worst part.

The worst part of the increase in government debt is the bill hasn’t even come due.

Federal debt may be up $10 trillion in eight years, but the cost of servicing that debt is about the same as it was in 2007, and as a share of the federal budget, interest costs are lower today than they were eight years ago.

A zero percent interest rate policy from Ben Bernanke and Janet Yellen plus trillions in debt monetization have made the borrowing binge painless.

But what happens when the bill comes due? Interest costs on the federal debt are likely to soar, hoovering up precious resources that could otherwise be used to return more of the money you send to Washington back to your pocket.