You don’t have to be able to predict the future to be a successful investor. But being armed with battle hardened advice can certainly help you become one.

From Richard C. Young’s Intelligence Report, July 2007 (subscription required):

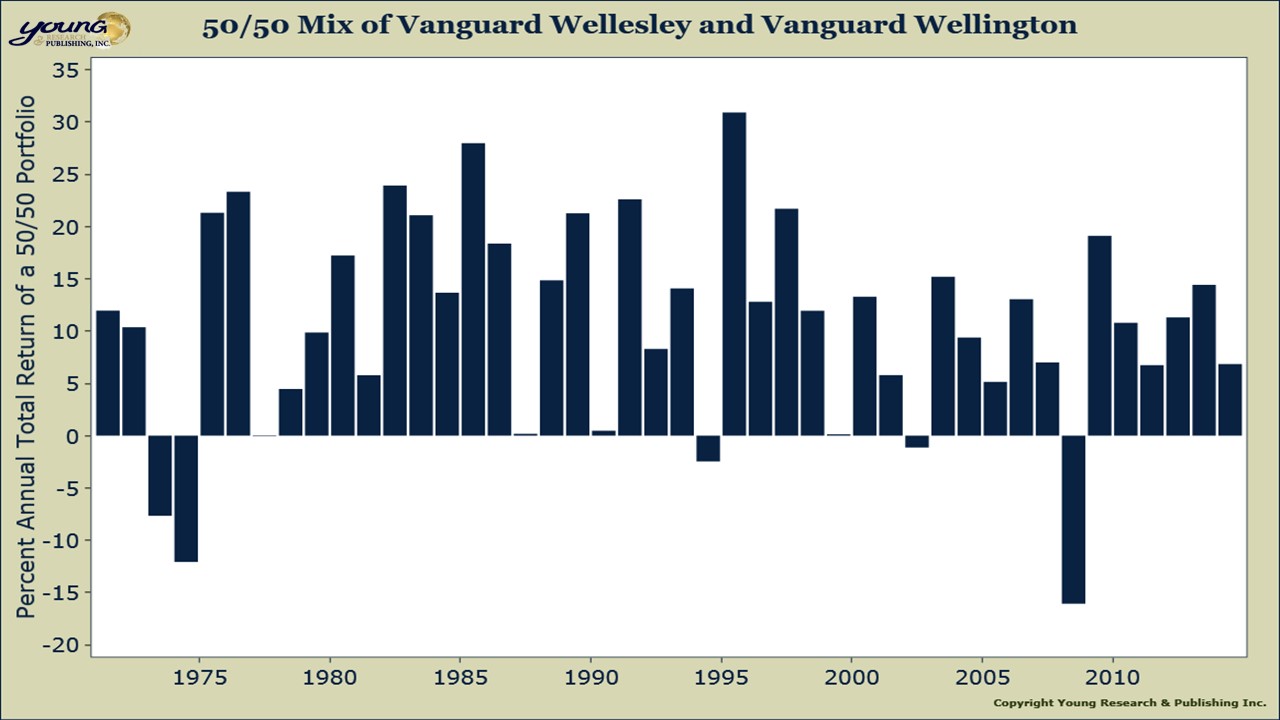

Your Portfolio Mix

At the start, retired investors and investors saving seriously for retirement (76 million boomers will begin retiring next summer) must answer two basic questions: (1) What is the proper mix of stocks and bonds? (2) How much money can be drawn annually from an investment portfolio? I have used Ibbotson data and examined 20-year rolling time periods from 1926 on. I have concentrated on minimum returns in order to advise a portfolio mix most likely to assure a draw of my advised 4%. The highest minimum return over 20-year rolling periods was achieved with a portfolio mix of 50/50 bonds and stocks. That minimum return was 4.6%. I would treat a 50% fixed-income portfolio component as suitable. And there is no way I’d go over 4% (inflation adjusted) for my annual draw. In fact, if possible, investors of suitable means are advised to cut back to a 3.5% draw (of an initial portfolio). Of course, the two best ways to make sure that you and your spouse do not outlive your money are to (1) work longer, and (2) slash your annual living expenses.